F45 Training is doing a SPAC. Time to check out IPO v DL v SPAC paradigm

F45 Training is doing a SPAC. Time to check out IPO v DL v SPAC paradigm

Understanding trade-offs issuer companies must consider while making the decision on the route they take to get listed - IPOs, Direct Listings or SPACs

Access to capital during a crisis can be a great motivator to get listed

There are multiple reasons why a company might decide to go public:

Creating a liquid market for its shares,

Raising its public profile, or

Providing an exit to early investors, among others.

But one particular benefit, which becomes very attractive, especially while witnessing a generational crisis like a pandemic, is the ability to access capital.

You may have noticed, Australia’s public markets have been buzzing in the last few months. Several companies reeling under the COVID-19 impact have been forced to raise capital to tide over short term liquidity concerns.

According to the AFR, $27 billion worth of capital raisings has been completed in Australia during the crisis. To put that in context - that represents half of the capital raised across the world, for an economy that barely accounts for 2% of the global GDP!

(Understandably, this has resulted in some very happy investment bankers - but I digress)

Looking at these markets, a private company in Australia could think to itself, ‘You know what, its certainly handy to be listed and have access to this large pool of capital’. It may even think ‘we are a fast-growing company with a great business model - why don’t we get listed?’

And that’s when they should start thinking: What approach do we take?

Most companies have no choice but to take the ‘conventional approach’

The IPO or Initial Public Offering is the process through which private companies offer their shares to the general public for the first time.

Now, till not too long ago (we are talking pre-2018) - there was only one viable approach to make this offering. In fact, for companies around the world, except in the US, there is still only one viable approach - the conventional approach.

Under the conventional approach the company or ‘issuer’ kicks-off preparations by forming an IPO Team, comprising investment banks/underwriters, legal counsel, accountants and other sundry experts. The investment banks quarterback the entire process of course, they

Write the prospectus and liaise with the regulator

Market the deal to investors

Price the deal after taking investor feedback

Make no mistake, this whole process is extremely demanding on the issuer company, and for the duration of the IPO process (6 - 8 months), it will generally become the issuer company CFO’s raison d'être.

So essentially the company jumps through hell to get their IPO done. However, as this was the only approach available, everyone bit their lips, got through the process and emerged victorious at the end to ring the bell. (don’t miss clicking on this link :)

Well almost everyone…

Barry McCarthy’s ‘hold my beer’ moment - how he defied the conventional approach

Barry McCarthy ( Spotify’s CFO at the time) decided to upend the conventional approach. In 2018, Spotify went public via the Direct Listing approach.

So what exactly is a Direct Listing?

Well, it’s pretty similar to the conventional approach in that you need a prospectus but differs significantly in how the deal is marketed and priced.

Here is Barry McCarthy summarising his view on the matter and my view of how Direct Listings resolved his issues

For a long time, I have watched the public market and thought that it was chronically broken. And I thought surely there must be a better way. So there were a couple of things I was trying to solve for

One is it's just an IPO without the ‘O.’ And we had a billion seven of cash, and which we couldn't even begin to deploy at the time, so if we had gone public, we would have sold 12 to 15 percent of the market cap in order to have the liquid secondary market, so it would have been a one-and-a-half, two-and-a-half billion dollar size transaction. For What?

Essentially, he is saying - ‘We have all the cash we need. We don’t want to suffer additional dilution by raising any cash that we don’t need’

The one major point of difference for direct listings is that - there is no offering - the issuer company does not raise any new capital in the process. It made sense. If the issuer company is swimming in cash, as Spotify was at the time (sitting on $1.7b) - do they need to raise more in an IPO and have the extra dilution?

He continues

Two, we wanted liquidity. In a traditional process, everybody gets locked up for 180 days; maybe that lockup gets staggered. It violated a core principle for us. I think we had 2,100 shareholders; we had employees who had owned the stock for a long period of time. We wanted them to have the opportunity to get liquid at the same time other shareholders were able to get liquid

The conventional approach provides liquidity to the existing shareholders. But unfortunately, there is a catch. The investment banks will generally require that all pre-deal shareholders commit to a six-month ‘lock-up’. In other words, after unloading the agreed number of shares in the IPO process, the pre-deal shareholders will commit to hold-on to their remaining shares for atleast six months after the IPO. This is to ensure there is no undue selling pressure on the stock. Of course, there is no such requirement for the investors who acquire the shares in the IPO, they can sell it the very next day.

Barry & co were trying to solve for this requirement, which it is interesting to note, is not imposed by law, but by industry convention. And he did, direct listings do not have any lock-up requirement for existing shareholders

Three, we had this core value around radical transparency. We’d been absolutely transparent with our private shareholders; we wanted to take the same approach with public shareholders.

Conventional IPOs have restrictions around forward-looking statements, the regulators do not want private companies dazzling retail investors with pie in the sky numbers and has strict guidelines on what an issuer company is allowed to say concerning future performance. While it is a lot of hassle to get this guidance published, the issuer company can take the less onerous option of briefing the large institutional investors in the 1x1 meetings. This would mean the retail investors might not have the same level of information, but they are price takers anyway.

Barry & co (especially Daniel Ek, co-founder of Spotify) wanted to make sure the same information was made available to everyone. A direct listing solves for this by granting issuer companies a one to two week window before official trading begins to publicly announce forward-looking guidance.

And then lastly, we wanted market-based price discovery. And every stock, including direct listing stocks, open exactly the same way. Every day

Matt Levine, Bloomberg columnist and overall finance guru gives us a good overview of how IPO pricing works in a conventional IPO

The way initial public offering pricing works is that investors want to buy stock in a new company at a low price, and the company wants to sell it at a high price, and an investment bank listens to both sides’ arguments and then tells the company what price it can sell the stock at, and the company generally does what the bank tells it to do.

On the other hand, the pricing mechanism used for direct listing is the same algorithm that is used by existing listed stocks to find the opening price on a daily basis. Sellers and buyers put in their order volume and value, a computer matches the offers and bids to determine the price at which the trade happens. No big deal.

The direct listing proponents thus make the case that there is no need for the ‘expert’ investment bank to price the deal.

And so, in April 2018 Spotify listed on the NYSE through a direct listing. On listing day, the shares experienced lower volatility compared to other large technology IPOs in the past decade.

Spotify had achieved all of Barry’s objectives, and they were not the only company to do it.

And then there were two - Slack IPOs using direct listing and the VC world goes ballistic

In 2019, Slack also took the direct listing approach to go public, driven by similar motivations and encouraged by Spotify’s success - it made the VC industry take serious notice.

It was like the eye of Sauron had suddenly noticed Frodo with the ring. The VCs realised that the investment banks had been ‘mispricing’ IPOs for decades.

In October 2019, Bill Gurley, famous VC investor and general partner of Benchmark Capital, gathered more than 100 CEOs of late-stage private tech companies and another 200 or so CFOs, venture capitalists and fund managers for an invitation-only event in San Francisco called “Direct Listings: A Simpler and Superior Alternative to the IPO.”

While the top three points listed by Barry were relevant to the VCs - the primary point of irritation was perhaps the pricing mechanism used in a conventional approach. The pricing “by hand” often resulted in something called the ‘IPO pop’.

The ‘IPO pop’ is the difference between the listing price of an issuer company and its closing price on day 1. Investment banks like to ensure that any stock which gets listed usually go up 10% to 20% or even more the next day. This helps to generate IPO buzz - investors are more likely to take a chance of investing in unknown companies if there is a sweetener of a quick gain. Lower the price, safer the deal - obviously from an underwriter’s perspective.

However, the problem it seems is that the investment banks are (under)pricing the deal so that the issuer companies and their VC backers end up leaving a lot of value on the table. Think about it, every dollar the price moves up after listing is a dollar return on investment lost by VCs - not to mention the additional equity dilution implied by the lower price.

You may be thinking, if this is a common occurrence, it would be useful to see how much money has been ‘lost’ by founders and VCs because of this mispricing.

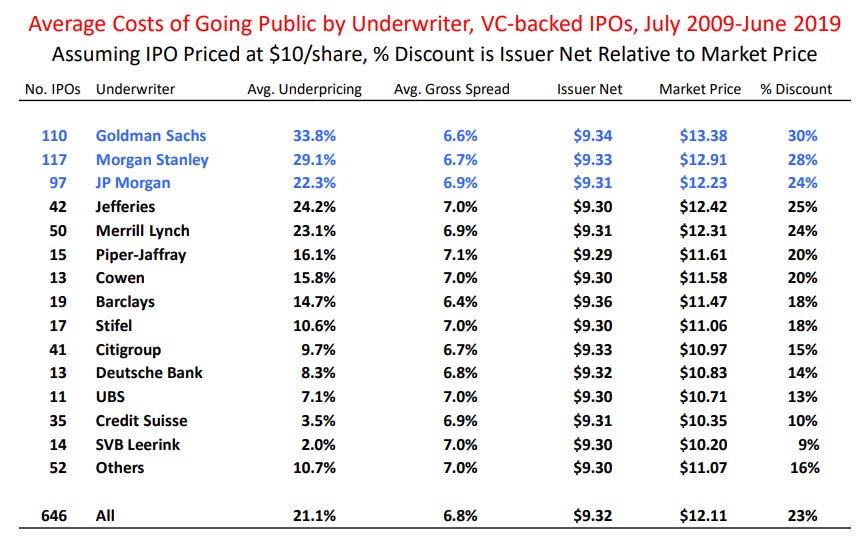

Luckily, Prof. Jay Ritter, an IPO expert at the University of Florida already has the answers

It looks like the best in the business - Goldman Sachs, Morgan Stanley - are not the best in the business from the issuer company’s point of view. These banks on average have underpriced IPO’s by 30% or more. From 1980 to 2018, underpriced deals have cost companies an estimated $165 billion. That implies a massive wealth transfer from VCs to institutional investors facilitated by the investment banks.

What’s more - the IPO fees payable to investment banks under the direct listing route are much lower as well. While in a conventional IPO the underwriting fees are in the range of 5-7%, direct listing only pays out 2-3% as advisor fees.

But what about the problem of not being able to raise any fresh capital?

Easy - just raise the capital in the private market before listing OR get listed and then raise capital once you are public. Treat the IPO as a liquidity event, not a fundraising event.

All this seems very attractive for potential issuer companies looking to go public. Pioneered by Spotify, followed by Slack and championed by VCs.

So you may wonder how many direct listings have happened since Slack?

Zero.

That’s because direct listings are not quite the ‘all-weather’ option that would work seamlessly even during uncertain times - like a pandemic.

But then, the markets looked around and found something useful from the attic.

F45 - The Australian fitness chain announced that it will get listed on the Nasdaq….

Founded in 2013, F45 operates 1,240 studios across 53 countries. It’s probably one of the fastest-growing fitness chains in the world. Its programs are based on heavy functional high-intensity interval and circuit training, a trendy approach that’s attracted celebrities and athletes around the world. Actor Mark Wahlberg is also one of the early investors in F45.

It recorded revenues of $93m in 2019 with a 33% adjusted EBITDA margin. The FY17-19 revenue CAGR was 91% and the adjusted EBITDA CAGR for the same period was 255%.

F45 WAS KILLING IT.

It even announced plans for a conventional IPO in January 2020.

And then, COVID-19 happened

Gyms were one of the hardest-hit sectors and the FY2020 financials got crushed. Suddenly there was a whole lot of uncertainty in the environment.

Source: SEC filings

With their gyms shut and questions hanging over the viability of a communal gym model in the post-COVID world, the management certainly wouldn’t want to go through the trouble of filing the prospectus, doing intensive roadshows and then see poor market sentiment or some sudden spike in COVID cases in one their key markets ruin their IPO.

The thing with the conventional IPO is that it’s not done till its done - in other words, there is no certainty till you actually get the cash in your account.

If only there were a way to get certainty. (remember what the markets found in the attic)

….via a SPAC (Special Acquisition Vehicle)

In June 2020, F45 announced that it had entered into a definitive agreement to merge with Crescent Acquisition Corp, a SPAC listed on the Nasdaq.

Okay, so what is a SPAC and how do they work?

A SPAC is an empty shell company or a blank check company that has raised a ton of money from the public (via a conventional IPO, btw) with the promise of finding and merging with an attractive target company. They are not like PEs which invest in multiple companies, a SPAC will only ever invest in one target. SPACs usually have a life of fewer than 24 months, within which they have to find the right target company or return the money to the investors.

A SPAC comprises of the sponsor (this is the person who does the work of looking for the target) and public shareholders (the folks who trust the sponsor with a blank check to find a target). The sponsor usually gets a shareholding of 20% in the SPAC as part of their fee (for offering expertise in finding the right target)

Interestingly, SPAC is not a new-fangled product. On the contrary, it is a dusty and grimy product that has been around since the 1980s and primarily seen as a way for smaller companies to tap the IPO market. It saw sporadic usage (with a peak in 2007), but hardly used post the GFC.

But then, it picked up steam in 2017 and has gone through the roof over the last 2 years.

Source: WSJ article

So what changed? How did a grimy old product become the hot new thing?

The movement was probably kicked off by Chamath Palihapitiya, the inimitable founder and CEO of Social Capital when he took Virgin Galactic public by merging it with his SPAC. With two more SPACs looking for targets, here’s his take

Our mission is to create an alternative path to a traditional IPO for disruptive and agile technology companies to achieve their long term objectives and overcome key deterrents to going public.

So here we go again…remember Barry McCarthy and his problems with the conventional IPO process...

Let's try to understand why a SPAC is attractive for certain IPO candidates

Transaction execution certainty

Here is Slack CEO, Stewart Butterfield’s take on capital raising environment

I’ve been in this industry for 20 years. This is the best time to raise money ever. It might be the best time for any kind of business in any industry to raise money for all of history, like since the time of the ancient Egyptians. It’s certainly the best time for late-stage start-ups to raise money from venture capitalists since this dynamic has been around.

That statement was made in 2015 when capital raising was a breeze.

In 2020, things are a bit different, to put it mildly.

Consider F45. Even a company with such strong fundamentals - fast-growth, a great business model and high profitability - would rather not chance market sentiment and take the conventional IPO approach. A SPAC provides them with the ability to enter into a definitive agreement and know for sure (for the most parts!) that the deal will not get pulled at the last minute.

Technically, once the terms are agreed between the target and the sponsor, it needs to be approved by the majority of SPAC shareholders. Remember how the sponsor gets a 20% shareholding - so you only need another 30% to make the cut. In other words, you only need 37.5% of the public shareholders to vote in favour of the deal. So it's quite likely that once the sponsor agrees on terms with a target - the deal will go through.

This is quite an attractive thing to have in uncertain times. Just ask WeWork.

One-stop negotiation

In a SPAC, a target company only has to negotiate with one party - the sponsor. They only have to convey their story to one party. There is no need to go around continent-hopping doing roadshows and pitching multiple institutional investors. Also, no shareholder ‘lock-up’ required!

It may be intense negotiation, but it’s a one-stop negotiation.

Lower bar to entry

F45 has 1,250 studios, $100m in revenues. It’s fine

Nikola Corp is a company with a promise of making electric trucks and zero revenues. It now has a market cap of $11b.

Virgin Galactic reported revenues of little under $250,000 in the first quarter of 2020. It has a market cap of $4.8b.

The target companies which otherwise would have found it hard to convince a wider group of investors about their plans to gain market share and path to profitability, only need to convince one sponsor and they can get listed.

In some cases, they actively benefit from the sponsor’s expertise or brand. VectoIQ, the SPAC that acquired Nikola Corp was headed by Stephen Girsky, a former Vice Chairman of General Motors.

So we had established that direct listings are cheaper than conventional IPOs. What about SPACs?

Here are Matt Levine and a spectacularly nicknamed investment banker clarifying. Turns out that you cannot escape paying the boatman to get you across the river Styx

Nevertheless, despite the testimony from Franky Four Fingers, SPACs have been the flavour of the season.

From our discussions, we can understand how issuer companies and banks may be motivated to embrace SPACs. But what about the investors?

Turns out they too are taking up this product with gusto, here are some reasons why that might be the case

SPAC sponsor’s brand

SPAC investors are in essence going long on the SPAC sponsor. They are thinking “I know Chamath, he is a good egg, he will find a great company and I will be a co-investor with him”

Call option mentality

The way the SPAC is structured, on the downside you make money market returns on your funds, on the upside you get to own a handpicked hotshot company (okay, maybe the company turns out to be a dud, but stop being so negative, mate)

FOMO

The mystery is tantalising, which company will the SPAC eventually acquire. The next one could be Spacex or Airbnb or Coinbase. But to spin the wheel you need to buy the stock.

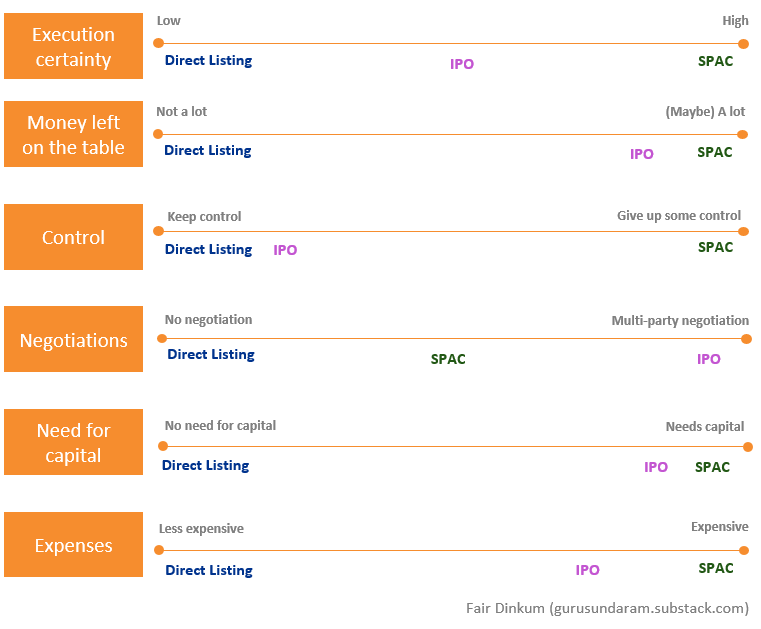

Okay, time to wrap things up…

The Going Public Paradigm: Relative level of importance accorded to these factors by the issuer company will determine the route they take go-public

The interplay of these factors with the economic climate of the time will drive the issuer company’s decision-making process.

In case of F45, they probably traded the execution certainty and the ability to negotiate with a single party offered by a SPAC against the better valuation and greater control of the company that they might have had under either a conventional IPO or Direct Listing option.

Are the conventional IPOs days numbered? Are SPACs the new normal? What about Direct Listings, will the proposal by NYSE to allow for capital raising make it more attractive?

Here’s my guess

More risky companies / early-stage private companies who would benefit from the stamp of approval provided by a reputed investor and don’t mind giving up some control - go down the SPAC route

Under a more benign market environment, late-stage private companies with comfortable cash position prefer to take the direct listing route

Conventional IPOs still remain the most popular route but with more and more companies asking the bankers to relax on ‘lock-up’ requirement and other vexations under the conventional IPO route

Only one thing is for sure - there are now new avenues in the going-public paradigm.