Crypto and Web3 saga

Crypto and Web3 saga

A roller-coaster year with all time highs, crazy twists & turns and trust-shattering low points

Crypto FUD - Is it now more real?

If 2021 was the year of ‘Up only’ for crypto - this year was much more of a reality check.

The unravelling started in May with the Luna collapse and was followed by bankruptcies at other major institutions including 3AC, Celsius, BlockFi, and Voyager.

As of end July the total cryptocurrency market cap was cut in half - down 55% since Jan 2022 - from $2.2 trillion to $1trillion. (In the same period S&P500 was down 17% and the Nasdaq was down 25%)

This upheaval was followed by months of unusual calm in the crypto markets. However, that ended in the first week of November when FTX spectacularly imploded.

By mid-December the crypto markets have contracted a further 15% to a market cap of c$850Bn.

However to put that in perspective, as of Jan 2021 - at the beginning of the bull run - the total crypto market cap was c.$750Bn.

So even with all the negative sentiment around crypto - the overall ecosystem is still valued higher than at the start of the bull run.

Re-discovering TradFi mistakes

Within the space of a few months - crypto has endured two massive crisis events.

Matt Levine, the Bloomberg columnist often says that the crypto industry is re-learning lessons from TradFi but on an accelerated timeline.

Act I: Crypto ‘GFC’

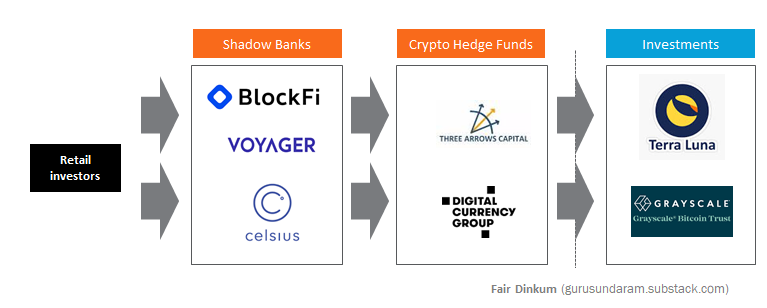

Building up all through the bull run and collapsing in May-June of 2022 - crypto managed to re-play a version of the Global Financial Crisis of 2008, complete with high levels of leverage and a system of opaque ‘shadow banks’.

There emerged a cohort of crypto firms like BlockFi, Voyager, and Celsius with a proposition to provide a “safe” rate of return to customers who deposit their crypto assets with these companies.

Essentially these entities were to operate like banks - taking deposits and lending them out, charging a high-interest rate, passing on the “safe” rate to the customers, and keeping the margin for themselves.

However, in the cypto world, unlike the real world, there aren’t a wide variety of people and businesses with real cashflows looking to borrow.

So most of these shadow banks had to lend their assets to hedge funds like 3AC (Three Arrows Capital)

By design - these hedge funds are the exact opposite of “safe” as they employ risky strategies to generate high returns. That is why they generally deploy their own capital or borrow from institutions that are supposed to have sophisticated risk/credit management teams.

But as you can see from the diagram above - the retail money was being funneled into such risky entities by a layer of shadow banks - in the name of providing a “safe” rate of return.

The investments/trades collapsed and the retail investors were left holding the bag.

This was a massive failure of risk/credit management by the ‘shadow banks’.

Here’s the story from CNBC in mid-2022

Three Arrows Capital managed about $10 billion in assets, making it one of the most prominent crypto hedge funds in the world….the firm, also known as 3AC, is headed to bankruptcy court after the plunge in cryptocurrency prices and a particularly risky trading strategy combined to wipe out its assets and leave it unable to repay lenders

Crypto exchange Blockchain.com reportedly faces a $270 million hit on loans to 3AC. Meanwhile, digital asset brokerage Voyager Digital filed for Chapter 11 bankruptcy protection after 3AC couldn’t pay back the roughly $670 million it had borrowed from the company. U.S.-based crypto lenders Genesis and BlockFi, crypto derivatives platform BitMEX and crypto exchange FTX are also being hit with losses.

This of course led many people to assume that crypto had failed - however, in reality, it was centralised crypto institutions (CeFi) that had actually failed…but DeFi worked as designed.. when everything was blowing up…DeFi worked as designed.

Here’s Airtree’s John Henderson

and Matt Levine

The DeFi platforms mostly did fine: They had collateral, they had automatic liquidation mechanisms, they liquidated the collateral, and they got their money back. The centralized lenders did less well. It turns out a lot were less strict about demanding collateral than you might have wanted

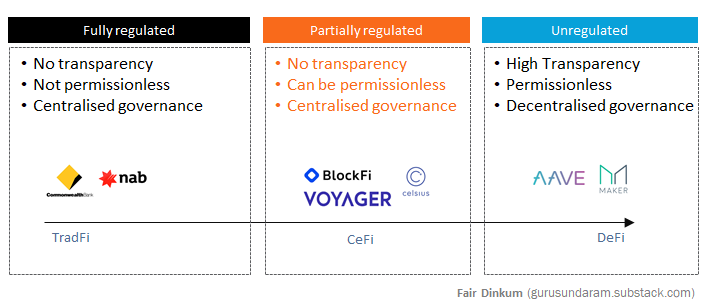

If we were to think of decentralisation based on the below factors..

i) Transparency: Ability for anyone to see details of loans, terms etc. (by being on-chain)

ii) Permissionless: Ability for anyone to join the platform as a lender/borrower

iii) Governance: Decentralised via a DAO or done more centrally by the management team

…we could come up with the below spectrum

You can then overlay the regulatory oversight on top

The TradFi banks are not transparent or permissionless and have centralised management - BUT they are fully regulated - there is really strong oversight via audits, mandatory disclosures, and very little room to engage in dodgy behavior.

On the other end of the spectrum are the DeFi firms like AAVE and MakerDAO - who all managed to come out of the market meltdown unscathed. These entities do not have regulatory oversight BUT have high transparency (all their loans can be tracked on-chain) and automated risk management which ensure above board behavior.

That leaves the shadow banks - in the gray zone - they are partially regulated and operate with very little transparency - allowing all kinds of horrendous behavior.

Act II: Enron + Maddoff

If that wasn’t enough excitement…crypto decided to do this

FTX is/was a centralized cryptocurrency exchange (CEX) founded in 2019 by Sam Bankman-Fried (SBF)

It was valued at US$32Bn in January 2022.

Now its worth zero. It has filed for bankruptcy. And SBF has been arrested.

Incidentally, here is John J Ray III, the administrator who oversaw the investigation into the Enron fraud and who is now in charge of the FTX liquidation

FTX lost $US8 billion of client money…

From compromised systems integrity and faulty regulatory oversight board, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.

… many FTX entities never held board meetings and the FTX group did not maintain centralised control of its cash…there were no accurate lists of bank accounts and not much attention was paid to the creditworthiness of banking partners. Ray has not been able to compile a list of who actually worked for the FTX Group.

It was a complete shit show.

The company failed to implement any transparency/ audit on its balance sheet, used its clients’ funds without their knowledge, and gave Alameda (its trading arm )special benefits.

This was a fraud - plain and simple.

What’s happening to Australian companies?

Not surprisingly these events have caused a massive trust deficit in the crypto ecosystem and Australian companies and investors have been caught in the cross-fire

c.30,000 Australian FTX customers directly affected

Other instances of companies impacted by the FTX fallout

Australian crypto exchange Swyftx laid off 35% of employees as a result of the crisis sparked by FTX’s implosion

Orthogonal Trading, a crypto hedge fund defaulted on $36m of loans on Maple Finance

Brisbane-based cryptocurrency broker Digital Surge has gone into voluntary administration. It was serving about 30,000 customers

But compared to what’s happening in the US - the fallout has been less severe in Australia.

Looking ahead

No doubt the crypto collapse and the aftermath will provide an ideal opportunity for regulators to formulate laws that would ensure investors are not caught again in a dodgy ecosystem like FTX.

Holding crypto assets in custody as a condition of an operating license is one of the central proposals in the Digital Assets (Market Regulation) Bill 2022 proposed by Liberal Senator Andrew Bragg.

It will be interesting to see how the regulatory regime evolves in Australia and in other jurisdictions next year.

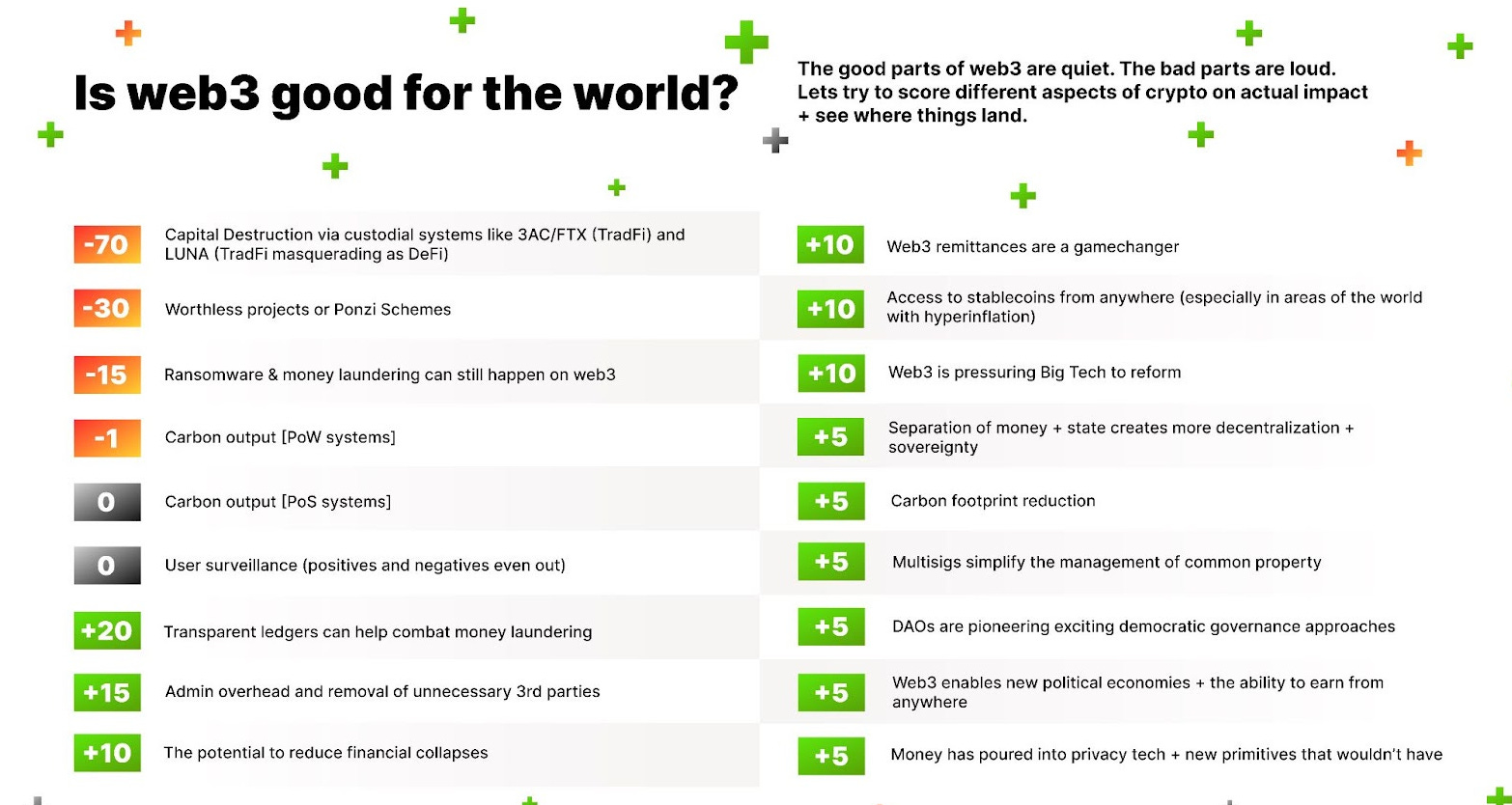

In the end I might leave you with a scorecard from Bankless attempting to capture the positive and negative social impacts of Web3

The takeaway here is not whether or not web3 is overwhelmingly good for the world right now, but that web3 has the incredible potential to regenerate the world if we continue to build upon web3’s positive impact opportunities.

The underlying message is - the bad parts of web3 have been very loud this year - however, the core technology still works and promises to provide many benefits to all of us.

On that note - wishing you all happy holidays and hope to see you all in the new year!